The REITweek 2025 convention on 6/2/25-6/5/25 served as an enormous data replace for a lot of the REIT sector:

- Contemporary working information as current as via the tip of Might.

- Administration commentary on immediately’s working atmosphere.

This text will focus on some key takeaways from the convention in addition to themes that resonate throughout a big portion of the REIT universe.

A focus of the REITweek convention was the huge disconnect between private and non-private actual property pricing. Actual property values have been growing in tandem with internet working earnings, so Web Asset Worth (NAV) of REITs has elevated. On the similar time, market costs of REITs have remained weak.

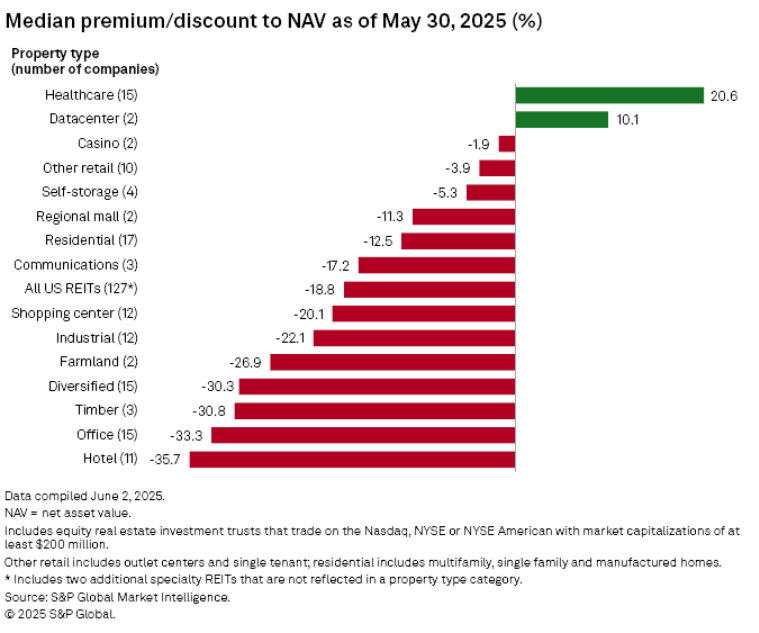

The disparate instructions of actual property worth and market costs has led to a unprecedented rift between asset worth within the non-public market and public inventory market caps. Reductions to NAV for every REIT sector are proven under:

{kind=link}

Healthcare is a little bit of an anomaly with corporations like Welltower (WELL) buying and selling at 190% of NAV. Premiums within the sector appear to be in names with at the least some publicity to senior housing. Fundamentals in senior housing are first rate, nonetheless rebounding from the previous crash, however I’m not satisfied everything of that premium is warranted.

Information facilities buying and selling at 110% of NAV is the results of AI pleasure. That’s reasonably easy. The market is anticipating continued development in information heart demand as AI rolls out and is pricing in a few of that development.

All the things else is discounted to asset worth. Some sectors are flippantly discounted whereas others are massively discounted. Everyone knows the distinction between top-down and bottom-up calculations, however given how giant these reductions are, one must hold that in thoughts when trying on the NAV low cost desk above.

A 20% low cost means 25% upside to NAV. A REIT buying and selling at a 33% low cost to NAV would wish to have its market worth enhance absolutely 50% simply to get to NAV. That’s the magnitude of disconnect between private and non-private actual property valuation.

This was the main level of debate on the REITweek convention. Most of the REIT executives had been instantly requested about their ideas on the disconnect and the way they may reap the benefits of it.

The reply was overwhelmingly share buybacks:

Crown Fortress (CCI) intends to funnel a good portion of its free cashflow into share buybacks.

Weyerhaeuser (WY) stated they accomplished a $1B buyback and teed up one other $1B buyback.

Potlatch (PCH) mentioned partaking in important share buybacks.

Kimco (KIM) has purchased again 3 million shares since 3/31/25 at a weighted common worth of $19.61.

Farmland Companions (FPI) per its 1Q25 earnings “repurchased 63,023 shares of its frequent inventory at a weighted common worth of $11.74 per share.” This adopted on from different buybacks through which they’ve purchased again greater than 20% of excellent shares

I may go on with myriad REITs shopping for again their inventory.

A 180-degree flip in REIT development patterns

The historic working sample of REITs is that they subject shares and use the recent capital to purchase extra properties. They used to develop by rising bigger.

Now, they’re rising by shrinking. They’re actively promoting property and utilizing the proceeds to buyback inventory.

Why?

All of it comes again to the huge disconnect between inventory costs and the worth of actual property.

NAV is the extra correct quantity. It represents the costs at which properties are literally transacting. Consensus NAVs are sometimes delayed as a result of it takes analysts some time to collectively modify their estimates, nevertheless it’s not onerous to seek out transaction information in actual time. For lots of the REIT sectors, actual time NAV is even greater than the consensus NAV as a result of property values are nonetheless rising.

In retail, for instance, non-public capital is clamoring over itself to get open air procuring facilities. There’s a whole lot of capital chasing not all that many properties on the market. Analysts are frequently elevating their NAV estimates, as seen under with Kimco, however costs are nonetheless rising past their newest figures.

S&P World Market Intelligence

The huge disconnect in worth between private and non-private gives REITs with a brand new technique to develop. They will promote property at their true worth and purchase again inventory at 60%-80% of honest worth.

These buybacks are instantly accretive to NAV and AFFO/share.

Shopping for again their inventory is the equal of shopping for a $500,000 home for $300,000. It’s such an apparent win and primarily based on the commentary from administration groups at REITweek, it appears the executives are diving into the chance. They know what their property are value and if the inventory market isn’t going to present them credit score, they may simply purchase it themselves. In so doing, it should drive additional NAV development and a share focus that can speed up AFFO/share development.

REITs have traditionally traded primarily in a spread of 90%-105% of NAV. It’s a current phenomenon that the index as an entire is buying and selling 20% low cost to NAV and plenty of corporations are buying and selling 30% and even 40% discounted to NAV.

Shopping for property up to now under the place they’re observably and measurably valued is a good alternative, however an investor nonetheless must know what they’re doing.

How you can discern when a reduction to NAV is really a possibility

We not too long ago mentioned the idea of reductions to NAV not essentially being alternatives with Hudson Pacific (HPP). You may learn the full evaluation right here, however the important thing concepts had been:

- Leverage could make low cost to NAV bigger than the true enterprise worth low cost.

- Declining asset worth could make low cost to NAV disappear the flawed means, the place NAV drops to market worth reasonably than market worth shifting as much as NAV.

The workplace sector is buying and selling at a 33% low cost to NAV. Think about the skyscrapers that make up the New York Metropolis skyline. These towers are clearly value a ton of cash and could be wildly costly to construct immediately, however they are not simply transactable. So even when a given workplace tower is value $1.2B within the theoretical sense, it could be troublesome to truly promote it for that a lot. It will get additional difficult when noting that rental charges and occupancy are doubtlessly declining, which may erode that theoretical $1.2B worth.

If the low cost to NAV is giant sufficient, it may possibly nonetheless work, nevertheless it’s messy and dangerous. As such essentially troublesome sectors like workplace, lodge and self-storage stay dangerous even with the reductions at which they’re buying and selling.

Shopping for REITs at a reduction to NAV is a a lot cleaner proposition in sectors the place there are elementary tailwinds. To actually reap the benefits of the dislocation between actual property values and the market worth of REITs I feel it is best to stay to areas with the next standards:

- Properties are transactable.

- Property values are persevering with to rise.

- Web working earnings of underlying properties is rising.

For my part, the 4 sectors with the best disconnects between private and non-private valuations that additionally meet the above 3 elementary standards are:

- Purchasing facilities – 20.1% low cost to NAV

- Industrial – 22.1% low cost to NAV

- Farmland – 26.9% low cost to NAV

- Timberland – 30.8% low cost to NAV

We already believed these sectors had been sturdy, however the recent information from REITweek additional demonstrated energy.

STAG Industrial (STAG) introduced its working outcomes all through Might 26.

STAG

In simply April and Might, STAG signed 4.5 million sq. toes of house at a 36.8% GAAP enhance to lease. That represents each an acceleration in leasing quantity and spectacular lease spreads.

East Group Properties mentioned at their REITweek assembly some visibility right into a constructive inflection level in industrial leasing as early as June 2025 (this month). If you understand the monitor report of EGP or its administration, they aren’t the sort of individuals to make empty guarantees. I’m keen to wager that they’ve good cause to imagine leasing is about to get even stronger.

Kimco (KIM) started its REITweek assembly discussing 4.4 million sq. toes of leasing with +49% money spreads. The remainder of the assembly was about sturdy tenant demand and shortage of provide of high-quality open-air procuring facilities.

I listened in on the conferences of each Weyerhaeuser (WY) and Potlatch (PCH) and the frequent chorus was that the upcoming enhance in duties on Canadian lumber from 14% to 34% goes to considerably enhance margins for American lumber producers. There could also be extra tariffs past the responsibility, however the responsibility alone is ample to revitalize mill margins. The businesses additionally mentioned the energy of timberland within the non-public market with even mediocre land buying and selling north of $2,000 per acre. The timber REITs, which have significantly better general land high quality, are buying and selling far under $2K per acre when adjusting for the worth of mills and inventories.

Farmland is among the most liquid onerous property. The worth of farmland is repeatedly measurable by the each day auctions that happen. It has a unprecedented monitor report of appreciation, and that development has not modified.

Wrapping it up

It isn’t simply my opinion that procuring facilities, industrial, timberland and farmland are excessive worth property. It is the consensus of trade members and verifiable by precise transactions, primarily in real-time.

The non-public worth of those property is cleanly determinable with fairly small error bars. Present market pricing of REITs is the true phenomenon. It isn’t sustainable for top of the range and rising property to commerce up to now under NAV.

Both the market worth will rise to strategy NAV, or the businesses will simply seize accretion via buybacks. Both means, I feel it is an awesome alternative, and we’re very lengthy the essentially sturdy but extremely discounted sectors.